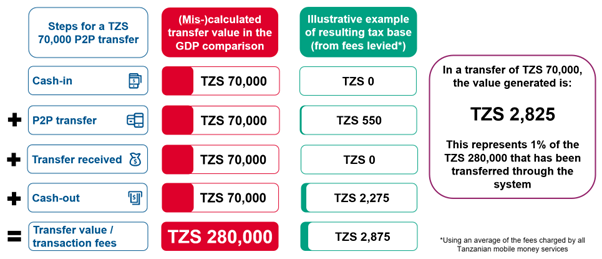

Last October, the Zambian government announced the imminent introduction of a tax on telephone transactions. The tax will specifically target payments between individuals and will range from 8 ngwee ($0.0038) to 1.80 kwacha ($0.085), depending on the size of the transaction.

Felix Mutati, Zambia's Minister of Technology and Science, said telephone transactions will rise to 170 billion kwacha ($6.5 billion) in 2022, up from 95 billion kwacha ($3.75 billion) in 2021. This should encourage the government to seize the opportunity presented by this booming sector to replenish government coffers.

"Negative effects, especially in informal sector”

This is not to everyone's taste. Some players in the sector expect negative repercussions, especially in the informal sector. Among them is Postle Jumbe, president of the Alliance of Zambia Informal Economy Association (AZIEA): "Imposing a tax on mobile money means that people will pay more. This could slow down the rapid digital transformation taking place in the country, characterized by the adoption of digital payment solutions.

According to a study by the Institute of Development Studies (IDS), "Taxing mobile money in Kenya: impact on financial inclusion", "while the amounts transacted may not change, users send and receive money within households less regularly. In addition, the tax seems to have a more detrimental impact on poorer households, which were less likely to be financially included before the tax was introduced. Larger households also show more negative effects after the tax.

"Taxing mobile money could have unintended consequences for the people who stand to benefit significantly from these platforms"

Similarly, pan-African telecoms operator Vodacom, which published a Mobile Money Taxation Report arguing for more lenient taxation of financial technology services, says: "While many countries have embraced mobile money services, mobile money taxation can have unintended consequences for the people who stand to benefit significantly from these platforms," said Stephen Chege, chief officer for regulatory and external affairs at Vodacom Group.

And it recalls the impact of mobile money on African societies. "For instance, mobile money platforms such as M-Pesa have been vital drivers of financial inclusion on the continent. However, government tax policies pose a significant challenge to the sustainability of mobile money services and financial inclusion gains made by these innovations."

"Disproportionate taxation measures cannot solve poorly formulated and administered tax policies in the long term. It can be argued that this approach reflects a misunderstanding of the mobile money industry and, consequently, an inaccurate assessment of the full impact of mobile money taxes," the report concluded.

“Mobile money in Africa is one of the most established and fastest growing financial technology sectors in the world”

Mobile money in Africa is one of the most established and fastest growing financial technology sectors in the world, according to statistics from the GSM Association's (GSMA) latest State of the Industry Report on Mobile Money 2023. "There are now 781 million registered mobile money accounts in sub-Saharan Africa, representing 48.8% of global users. Sub-Saharan Africans registered 17% more accounts in 2022 than in 2021, with the value of transactions reaching $836.5 billion. Globally, mobile money transactions exceeded $1,260 billion.

Of the 781 million active accounts in Africa, 763 million are in sub-Saharan Africa, with the remaining 18 million registered in North Africa. The report concludes that this growth spurt is due to regulatory changes in sub-Saharan Africa that have led to the rapid development of mobile money services. However, new tax policies must not be allowed to slow this growth.